What is this commitment?

This is a collective commitment by a leading group of companies to strengthen and align climate-related corporate reporting to the investment community through a common framework, by pledging to implement the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), convened by the G20 Financial Stability Board.

More fundamentally, it is a recognition that, because climate change is beginning to affect economic activity in various ways, it has become a relevant matter for consideration by fiduciaries irrespective of how they view its moral or societal implications.

The commitment was launched following the release of the TCFD recommendations. The full list of committed organisations can be found here.

What is the purpose of this commitment?

The purpose of this commitment is to:

Articulate a shared commitment by an influential initial coalition of companies to begin to implement the TCFD recommendations and report climate-related financial information in mainstream filings through the Climate Change Reporting Framework or other comparable frameworks, whether or not required by current regulation.

Demonstrate market support behind the TCFD recommendations and willingness to contribute to managing the risks of climate change to financial markets through better reporting; and

The expectation is that once this opinion-shaping coalition of first-mover firms begins to report on a common and comparable basis to their investors, this will create a demonstration effect within the wider corporate and financial communities, and lead eventually to the scaled incorporation of climate-related corporate performance and risk considerations into routine capital allocation decision making within the financial system.

Why now?

Following the release of the final TCFD recommendations, the next step is for a leading group of businesses to lead by example and begin the implementation of these recommendations into their reporting requirements.

The theory of change behind this commitment is that once best practice is established, the market will follow and reporting in line with the TCFD recommendations will become standard market practice.

Who coordinates this commitment?

The commitment is coordinated by the Climate Disclosure Standards Board (CDSB) and supported by the We Mean Business Coalition, CDP, Ceres and others.

CDSB is an international consortium of business and environmental NGOs committed to advancing and aligning the global mainstream corporate reporting model to equate climate change and natural capital with financial capital.

CDSB does this by offering companies a framework for reporting environmental information with the same rigour as financial information. In turn this helps them to provide investors with decision-useful climate change and environmental information via the mainstream corporate report, enhancing the efficient allocation of capital. Regulators also benefit from compliance-ready materials.

Recognising that information about natural capital and financial capital is equally essential for an understanding of corporate performance, CDSB work builds the trust and transparency needed to foster resilient capital markets. Collectively, CDSB aims to contribute to more sustainable economic, social and environmental systems.

CDSB Board Members are:

CDP (Secretariat)

Ceres

The Climate Group

The Climate Registry

International Emissions Trading Association

Sustainability Accounting Standards Board

World Business Council for Sustainable Development

World Economic Forum (Chair)

World Resources Institute

What is required to make the commitment?

The following criteria must be fulfilled in order to make this commitment:

- A company listed on an exchange (exceptions may be made)

- The company is willing to report in line with the TCFD recommendations, as outlined in the commitment

Is there a cost to make the commitment?

No, there is no cost associated with making the commitment.

Where can I get support with implementing the recommendations?

CDSB will be actively providing committed companies with resources to learn more about the recommendations through webinars, workshops and by developing guidance. Committed companies can also get in touch with the CDSB Secretariat by emailing with specific questions.

For more tailored support, committed companies may wish to get in touch with advisory firms, such as those on the CDSB Technical Working Group.

How can my company sign up?

If you would like to become a signatory, fill out this form or get in touch with the CDSB Secretariat by email at or phone at +44(0)782 540 9060.

There are a lot of TCFD-related statements, how is this different?

The statements and this commitment have been part of a single, coordinated effort to show business leadership and support of the TCFD’s recommendations.

The statements by the World Economic Forum, We Mean Business Coalition and the TCFD themselves have all been crucial at key stages of the global dialogue on the Task Force on Climate-related Financial Disclosures (TCFD). They have all served the same purpose: to send a clear signal to governments that the private sector supports the remit and work of the TCFD.

As the final recommendations are released, the time is right for companies to start implementing the body of work that this initiative has produced and drive forward the global agenda on climate resilience through disclosure.

The CDSB commitment on the TCFD recommendations aims to showcase the actions of a leading group of businesses that are ready to integrate the recommendations and to support them on their journey.

I plan to implement the recommendations anyway. Why should I make this commitment?

The commitment offers three main benefits to companies planning to implement the TCFD recommendations:

- Safety in numbers: evidence of a group of companies implementing the recommendations creates a safe environment and eliminates many of the concerns associated with being a first mover.

- Support network: companies who make the commitment will be supported in the implementation process by CDSB, a non-profit consortium with 10 years of experience of climate change reporting in mainstream filings.

- Visibility: CDSB has partnered with the We Mean Business Coalition and others to bring visibility to the leadership of the companies who make this commitment.

The commitment itself is supported by a global campaign to show this growing corporate support of the TCFD recommendations to other companies, the investment community and governments.

What is the difference between the fiduciary duty statement and this commitment?

This commitment is the next iteration of the Statement on fiduciary duty statement & climate change disclosure. Both share a core element: the commitment to integrate consistent climate-related information within the mainstream report.

The main change since the previous statement and the current commitment is the specific focus on the implementation of the TCFD recommendations.

The purpose of the fiduciary duty statement was to articulate:

- A shared concern that financial markets do not take sufficient account of climate-related risks and opportunities relevant to future shareholder value due, in significant part, to insufficiently comprehensive and comparable climate change-related information in mainstream corporate reports;

- A shared commitment by an influential initial coalition of companies and institutional investors to begin to produce and use such information in mainstream reporting through the Climate Change Reporting Framework or other comparable frameworks, whether or not required by current regulation.

This core purpose has not changed and this update is only intended to make this commitment up to date with recent developments.

What is an “annual report or mainstream corporate filing”?

Although there are many different terms to describe them, this refers to the annual reporting packages in which certain organizations are required to deliver their audited financial results under the corporate, compliance or securities laws of the territory or territories in which they operate.

Mainstream financial reports are normally publicly available. They provide information to existing and prospective investors about the financial position and financial performance of the organization and are distinct from material published separately. Although a full list of these is beyond the scope of this FAQ, some example terms that are used in various jurisdictions are:

- Annual report

- Form 10-K or Form 20-F (USA)

- Management Discussion & Analysis

- Directors Report and/or Strategic Report (UK)

- Lagebericht

- Form 56-1 (Thailand)

What is the CDSB Climate Change Reporting Framework?

The Climate Change Reporting Framework sets out an approach to incorporating climate change related information into mainstream corporate reports. It adopts relevant principles from the existing mainstream corporate reporting model, including corporate governance and financial reporting principles. The CDSB Reporting Framework can be found here.

The Climate Change Reporting Framework is designed to convey climate change-related information of value to investors in mainstream financial reports. Created in line with the objectives of financial reporting and rules on non-financial reporting, the CDSB Framework seeks to filter out what is required to understand how climate change affects a company’s financial performance. Building on the work of its Board members, CDSB seeks to standardize environmental disclosures through collaboration and by identifying and coalescing around the most widely shared and tested reporting approaches that are emerging around the world. CDSB therefore adopts relevant principles from existing standards and practices with which business is already familiar. Through a process of continuous improvement and collaboration, CDSB has developed its Framework and associated guidance material for use by companies when making disclosures in, or linked to, their mainstream financial reports about the risks and opportunities that climate change presents to their strategy, financial performance and condition.

What are "other comparable frameworks"?

The commitment includes that signatories “…aim to produce such information on a common and consistent basis by applying the applicable frameworks, such as the CDSB Climate Change Reporting Framework* and others.”

Although the Climate Change Reporting Framework is unique in providing guidance on the integration of climate change-related information into mainstream filings in a consistent basis for an investor audience, other frameworks may be helpful for companies in delivering on this commitment.

For example:

Companies can disclose climate change and elements of environmental information through the CDP platform, which provides the structure for data collection and the content for reporting. The CDSB Framework then provides the guidance to communicate that content in mainstream reports, which helps companies inform their investors and stakeholders, while providing regulators with a comprehensive set of information.

The Sustainability Accounting Standards Board (SASB) provides a series of standards to reporting companies from all sectors, referencing the CDSB Framework for environmental information and natural capital reporting as further guidance for certain environmental metrics.

The International Integrated Reporting Framework enables a business to bring these elements together through the concept of 'connectivity of information', to best tell an organization’s value creation story. The CDSB Climate Change Reporting Framework is fully aligned with the <IR> Framework and provides more detail specifically on how to integrate climate change-related information in mainstream reports.

Other reporting frameworks and standards may also be helpful to companies in implementing the TCFD Recommendations.

What are the TCFD core elements?

The core elements of the TCFD’s recommendations are:

- Governance: Disclose the organization’s governance around climate-related risks and opportunities.

- Strategy: Disclose the actual and potential impacts of climate-related risks and opportunities on the organization’s businesses, strategy, and financial planning.

- Risk Management: Disclose how the organization identifies, assesses, and manages climate-related risks.

- Metrics and Targets: Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities.

These core elements are explained in more detail in the TCFD recommendations report, available here.

Do I need to completely implement the TCFD recommendations within 3 years?

Implementing all of the TCFD’s recommendations at a level that is appropriate to be included in the mainstream filing of a company will most likely take several reporting cycles for any company. In addition, some aspects of the recommendations (such as those relating to certain sectors) may not be applicable to all companies or following an assessment, certain information may be found to be immaterial to the company.

As such this is a commitment to implement the TCFD recommendations as fully as practicable, rather than in full. However, a continuous effort of alignment with the TCFD recommendations is expected from signatories to this commitment.

The 3 year time horizon stems from the time constraints associated with a smooth and orderly transition to a low-carbon economy, in line with scientific consensus and research conducted by prudential regulatory bodies such as the UK Prudential Regulatory Authority, European Systemic Risk Board and others.

A report by the UN Environment Finance Initiative highlights that, among others, pre-2020 climate change mitigation action:

- Supports the transition towards a least-cost emissions reduction trajectory after 2020 that is consistent with the well below 2°C target.

- Is likely the last chance to keep the option of limiting global warming to 1.5°C in 2100 open, as all available scenarios consistent with the 1.5°C target imply that global greenhouse gas emissions peak before 2020.

The intention of this timeframe is therefore to support the first group of committed companies to implement the TCFD recommendations by 2020. Companies committed at a later day will also be encouraged to keep to a three year timeframe.

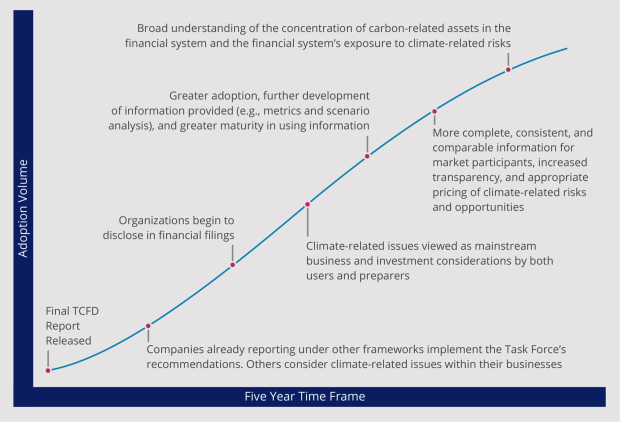

What is the TCFD’s implementation path?

The TCFD has outlined a five-year time frame for market adoption of its recommendations, as shown below. The time frame accounts for the process of year on year development and experimentation by reporting entities, which results in “More complete, consistent, and comparable information for market participants…” and finally a “Broad understanding of the concentration of carbon-related assets in the financial system and financial system’s exposure to climate-related risks”. Committed companies are expected to keep this pathway in mind as they implement the TCFD’s recommendations.

Image credit: Task Force on Climate-related Financial Disclosures